DEPARTMENT OF FINANCE

Office of Unclaimed Property, State Escheator

FINAL

ORDER

104 Department of Finance Abandoned or Unclaimed Property Reporting and Examination Manual

SUMMARY OF REGULATION

This regulation amends the existing regulation by making non-substantive changes to the description of agency organization, operations and procedures for obtaining information.

STATUTORY AUTHORITY

12 Delaware Code, Section 1132: “…[T]he State Escheator may make such rules and regulations as the State Escheator may deem necessary to administer and enforce this chapter.”

29 Delaware Code, Section 10113(b)(1) exempts regulations from the procedural requirements of Chapter 101 if the changes are “[d]escriptions of agency organization, operations and procedures for obtaining information.”

PROCEDURAL HISTORY AND FINDINGS OF FACT

The Department of Finance, acting through the State Escheator, adopted Regulation 104, Department of Finance Abandoned or Unclaimed Property Reporting and Examination Manual effective October 11, 2017. That Regulation contained contact information for the Office of Unclaimed Property which has since changed.

THEREFORE IT IS ORDERED, under the above-described statutory authority, and for the reasons set forth above, I hereby ORDER that the revisions to 12 DE Admin. Code 104: Department of Finance Abandoned or Unclaimed Property Reporting and Examination Manual, be adopted and promulgated as follows, to wit:

1. Subsection 1.1 Contact Information for Holders shall be modified by removing the email address,

“escheat.holderquestions@state.de.us” and replacing it with “escheat.holderquestions@delaware.gov.“

2. Subsection 1.1 Contact Information for Holders shall be modified by removing the website address,

“http://revenue.delaware.gov/unclaimedproperty.shtml,” and replacing it with “https://unclaimedproperty.delaware.gov.”

3. Subsection 1.2 Contact Information for Owners and Claims shall be modified by removing the email address,

“escheat.claimquestions@state.de.us,” and replacing it with “escheat.claimsquestions@delaware.gov.”

4. Subsection 1.2 Contact Information for Owners and Claims shall be modified by removing the website address,

“http://revenue.delaware.gov/unclaimedproperty.shtml,” and replacing it with “https://unclaimedproperty.delaware.gov.”

The effective date of this Order is ten (10) days from the date of its publication in the Delaware Register of Regulations, in accordance with 29 Del.C. §10118(g).

Brenda M. Mayrack, State Escheator

Department of Finance

104 Department of Finance Abandoned or Unclaimed Property Reporting and Examination Manual

Introduction

On February 2, 2017, the Governor of Delaware signed into law Senate Bill 13 of the 149th General Assembly, which revised and updated the Delaware Abandoned or Unclaimed Property Law. On June 29, 2017, the Governor signed into law Senate Substitute 1 for Senate Bill 79, which further updated the Delaware Abandoned or Unclaimed Property Law and clarified portions of Senate Bill 13.

Section 1176(b) states as follows:

The Secretary of Finance, in consultation with the Secretary of State, shall, on or before December 1, 2017, adopt regulations regarding the method of estimation to create consistency in any examination or voluntary disclosure. These regulations must include permissible base periods, items to be excluded from the estimation calculation, aging criteria for outstanding and voided checks, and the definition of what constitutes complete and researchable records.

Statutory Authority

12 Del.C. §1132 Rule-making.

Except as provided in §§1167, 1173(a), and 1176(b) of this title, the State Escheator may make such rules and regulations as the State Escheator may deem necessary to administer and enforce this chapter.

These Regulations replace the following existing provisions in the Delaware Administrative Code:

12 DE Admin. Code 100, Regulation on Practices and Procedures for Appeals of Determinations of the Audit Manager

12 DE Admin. Code 101, Regulation on Practice and Procedure for Establishing Running of the Full Period of Dormancy for Certain Securities and Related Property

12 DE Admin. Code 102, Regulation on Practices and Procedures for Records Examinations by the State Escheator

12 DE Admin. Code 103, Abandoned or Unclaimed Property Examination Guidelines

These Regulations replace the following existing Regulations:

Abandoned or Unclaimed Property Voluntary Disclosure Agreement and Audit Program, 9 DE Reg. 771 (11/01/05).

Abandoned or Unclaimed Property Voluntary Disclosure Agreement Program, 10 DE Reg. 699 (10/01/06) (Final).

Regulation on Practices and Procedures for Appeals of Determinations of the Audit Manager, 15 DE Reg. 1323 (03/01/12) (Final).

Regulation on Practice and Procedure for Establishing Running of the Full Period of Dormancy for Certain Securities and Related Property,15 DE Reg. 1330 (03/01/12).

Regulation on Practices and Procedures for Records Examinations by the State Escheator, 16 DE Reg. 530 (11/01/12) (Final).

Abandoned or Unclaimed Property Audit Examination Guidelines, 16 DE Reg. 630 (12/01/12) (Final).

Regulations

1.1 Contact Information for Holders

Mailing Address: Delaware Department of Finance

Office of Unclaimed Property

8th Floor

820 North French Street

Wilmington, DE 19801

Phone Number 302-577-8782

Fax Number: 302-577-7179

E-mail: escheat.holderquestions@state.de.us escheat.holderquestions@delaware.gov

Website: http://revenue.delaware.gov/unclaimedproperty.shtml https://unclaimedproperty.delaware.gov

1.2 Contact Information for Owners and Claims

Mailing Address: Delaware Department of Finance

Office of Unclaimed Property

8th Floor

820 North French Street

Wilmington, DE 19801

Phone Number: 302-577-8782

E-mail: escheat.claimquestions@state.de.us escheat.claimsquestions@delaware.gov

Website: http://revenue.delaware.gov/unclaimedproperty.shtml https://unclaimedproperty.delaware.gov

2.1 Preface

The Department of Finance's Office of Unclaimed Property ("DOF" or the "State") is committed to promoting Holder compliance. Holders of abandoned or unclaimed property reportable to the State of Delaware must file annual reports and remit property to the State of Delaware. To encourage compliance and to enforce the State's Abandoned or Unclaimed Property Law, Title 12, Chapter 11 of the Delaware Code (the "Abandoned or Unclaimed Property Law"), DOF recognizes the need to conduct examinations. DOF recognizes that each examination is unique. This manual is intended to create a framework so that a Holder undergoing an examination by the State of Delaware will have a basic understanding of the process and the State's expectations. The standards contained in this manual are to be implemented consistently to ensure fair and uniform treatment of Holders. Absent permission from the State Escheator, the standards are not discretionary, and third-party audit firms may not develop or utilize their own distinct applications of these standards and instructions.

2.2 Guiding Principles

2.2.1 The goal of an unclaimed property examination shall be to determine whether the Holder is in compliance with the Delaware abandoned or unclaimed property laws. These examination guidelines shall relate to all property that may be subject to escheat pursuant to the Abandoned or Unclaimed Property Law of Delaware, Title 12, Chapter 11, of the Delaware Code. Abandoned or unclaimed property is reported to the State of Delaware pursuant to the Abandoned or Unclaimed Property Law and the priority rules and other provisions set forth in the United States Supreme Court case Texas v. New Jersey, 379 U.S. 674 and 380 U.S.518 (1965) and reaffirmed by Delaware v. New York, 507 U.S.490 (1993).

2.2.2 The State of Delaware has jurisdiction over the escheatment of property that has met one of three criteria:

2.2.2.1 The last known address of the owner is located in the State of Delaware;

2.2.2.2 The last known address of the owner is unknown, and the Holder is incorporated or formed under the laws of the State of Delaware; or

2.2.2.3 The last known address of the owner is not located in any state of the United States, or the District of Columbia, or any territory or possession of the United States, and the Holder is incorporated or formed under the laws of the State of Delaware

2.2.3 The State Escheator shall not use collection goals or quotas during the conduct of an examination to assess a Holder's compliance.

2.2.4 The State Escheator shall make available, upon request, copies of all contracts between the State Escheator and any third-party auditor hired to conduct or assist with an examination.

2.2.5 The State's goal in every examination is to be predictable, fair, and consistent while determining the Holder's historical compliance, and to encourage and facilitate the Holder's ongoing and future compliance with the Abandoned or Unclaimed Property Law.

2.2.6 The DOF is committed to promoting Holder compliance. In an effort to accomplish this objective, a Voluntary Disclosure Agreement (VDA) program has historically been available through DOF to Holders who may not be presently in compliance but want to comply with the Abandoned or Unclaimed Property Law. Currently, the Secretary of State administers a VDA program for Holders to come forward and report abandoned property liability. The agreement entered into at the conclusion of the VDA program releases Holders from all claims, demands, interest, penalties, actions or causes of action related to all property reported properly under the terms of the VDA.

2.3 Effective Date

The effective date of these Regulations shall be the date they are adopted, and the standards contained therein shall apply to all examinations commenced after that date. To the extent practical, the Regulations shall apply to any ongoing examinations that commenced prior to the effective date of these Regulations, though the failure of the State to have conformed to a Reporting and Examination Manual not-yet-in-existence would not invalidate an examination.

2.4 When property presumed abandoned

2.4.1 See Title 12, Chapter 11 of the Delaware Code for applicable dormancy periods for various property types.

2.4.2 For a stored value card or gift card, the maximum cost is determined utilizing information from an annual federal income tax return (for example, the 2016 Form 1120 or equivalent) for each applicable year. The State shall consider the cost of goods sold plus total deductions less charitable contributions, depreciation and depletion.

2.4.2.1 For example, an appropriate calculation would be as follows: for a corporation filing an IRS Form 1120 - U.S. Corporation Income Tax Return, the State shall use the following lines from Form 1120 to calculate maximum cost:

Line 2 COGS

+ Line 27 Total Deductions

- Line 19 Charitable Contributions

- Line 20 Depreciation

- Line 21 Depletion

Maximum Cost in Dollars

The Maximum Cost in Dollars divided by Line 1 Gross Receipts equals the Maximum Cost as a Percentage of Gross Receipts.

2.4.2.2 Other reasonable alternative calculations may be proposed by a Holder and shall be considered on a case-by-case basis by the State Escheator.

2.5 Indication of Owner Interest in the Property

2.5.1 Section 1136 of Title 12, Delaware Code defines various owner actions which constitute an "indication of owner interest in property."

2.5.2 Actions which do not indicate the owner's interest in the property include, but are not limited to, automatic postings, automatic reinvestments, computer system conversion dates and non-return of mail (other than a non-returned IRS Form 1099 for ACH or Dividend Reinvestment accounts).

2.5.3 A Holder may cross-reference an indication of interest in one investment or account with another investment or account with the same Holder if the records of the Holder indicate the same name on the account, signature card or contract.

2.5.4 Proof to the satisfaction of the State Escheator that an Owner has had contact with a designated representative of the Holder in the period of dormancy may be considered an indication of owner interest in the property.

2.6 Report Required by Holder

2.6.1 As of November 10, 2015, the State no longer accepted paper reports. The State will continue to accept reports in an electronic format through February 28, 2018. Beginning March 1, 2018, reports shall be required to be submitted in a web-based record.

2.6.2 Although not required by the Abandoned or Unclaimed Property Law or regulation, negative reports will be accepted from any person.

2.7 When Report to be Filed

2.7.1 Beginning February 1, 2018, to ensure a timely response by the DOF, a Holder's request to extend the date for filings shall be made a minimum of 15 calendar days prior to the date specified for the Holder under 12 Del.C. §1144.

2.7.2 The State Escheator may grant an extension of the date of filing for good cause. Good cause includes, but is not limited to, a natural disaster, criminal activity related to the Holder's books and records, recent changes in the form of ownership of the Holder through merger, acquisition or reorganization, and, for a Holder having three or fewer employees, a recent change in management. Beginning February 1, 2018, good cause shall not include a failure to perform a requirement such as due diligence pursuant to §§1148 and 1149 of the Abandoned or Unclaimed Property Law.

2.8 Address of owner to establish priority

In order to establish priority, a sufficient description or code shall include two of the following three data points, which must not conflict with each other: a City, a State or foreign code, and a postal code. The location of the transaction is not evidence of the last known address of the owner.

2.9 Retention of Records by Holder

Records to be retained by the Holder include the date, place, and nature of the circumstances that gave rise to the property right. These records may include the following: tax returns (including consolidated and affiliation schedules), organization charts, charts of accounts, unclaimed property filing history (for all states if the Holder is incorporated or formed in the State of Delaware), prior completed and accepted voluntary disclosure agreements (VDAs) and examinations, bank statements, bank reconciliations, outstanding check lists, detail general ledgers, aged accounts receivable reports, aged accounts payable reports, policies and procedures related to record retention, accounting, and unclaimed property, and if applicable, information surrounding gift card issuances and redemptions.

2.10 Authority to Conduct Abandoned Property Examinations

2.10.1 Section 1171 of Title 12, Delaware Code provides the State Escheator with the authority to examine the records of a person or the records in the possession of an agent, representative, subsidiary, or affiliate of the person under examination in order to determine whether the person complied with the provisions of the Abandoned or Unclaimed Property Law.

2.10.2 Section 130 of the Epilogue to the State's Budget for Fiscal Year 2018 (ending June 30, 2018) provides the Secretary of Finance or his or her designee with the authority to enter into agreements with organizations to identify abandoned property to be escheated to the State by means of audit, examination or otherwise. Similar, if not identical, language has appeared in the State's budget for decades.

2.11 Examination of Holders

2.11.1 The State of Delaware shall examine selected Holders' books and records for compliance with the Abandoned or Unclaimed Property Law. The examination shall be assigned to an auditor or to a third-party auditing firm ("Auditor" or the "Auditors") that has been retained by the State for such purposes. At the request of a Holder, and if the parties agree on the terms, the State's third-party Auditor shall enter into a confidentiality agreement with the Holder in a form approved by the State Escheator before any of the Holder's confidential records are produced. (See subsection 2.14, Confidentiality and Non- Disclosure Agreement, for a form NDA approved by the State.)

2.11.2 Pursuant to the State Escheator's authority to conduct an examination of the records of a Holder, the State Escheator possesses the authority to resolve an examination via negotiation and settlement with a Holder or their duly authorized representative. This authorization provides flexibility to both the Holder and the State to resolve issues that could require formal appeal or litigation. A mutually-agreed upon settlement resolves an examination as a whole and does not create any precedent on specific legal issues.

2.11.3 The State's goal in every examination is to be predictable, fair, and consistent while determining the Holder's historical compliance, and to encourage and facilitate the Holder's ongoing and future compliance with the Abandoned or Unclaimed Property Law.

2.12 Notice of Examination

2.12.1 All State of Delaware unclaimed property examinations begin with an official Notice of Examination letter from the State's Abandoned Property Audit Manager. The letter shall notify the Holder that its books and records (including those belonging to subsidiary and related entities) are subject to examination, identify the assigned Auditor, and include Auditor contact information. The issuance of the official Notice of Examination letter terminates the Holder's ability to enter into a VDA with the State of Delaware until the examination is concluded pursuant to the Abandoned or Unclaimed Property Law.

2.12.2 Third-party Auditors are not authorized to engage in any examination or audit without prior consent from the State of Delaware, Department of Finance.

2.12.3 Effective July 1, 2015, the State Escheator shall not initiate any new examination of records or an investigation of any person pursuant to the Delaware Abandoned or Unclaimed Property Law unless first the person has been notified in writing by the Secretary of State that the person may enter into an unclaimed property voluntary disclosure agreement, except in the following circumstances: (i) as provided in 12 Del.C. §1172(d), or (ii) if the person fails to otherwise comply with a requirement imposed on such person pursuant to §1173 of the Delaware Abandoned or Unclaimed Property Law.

2.12.4 The State is permitted to examine a Holder for any reason under the Abandoned or Unclaimed Property Law. When identifying a Holder to be examined, the State may consider several factors. These include, but are not limited to the following:

2.12.4.1 A review of past Holder reports for inconsistencies, omissions or a lack of detail;

2.12.4.2 A comparison of a Holder's past reports to the reports of similar Holders within the same industry and of the same approximate size;

2.12.4.3 Any information available from the State, such as Holder reporting and compliance history; and

2.12.4.4 Available public data regarding the Holder, including without limitation, annual company reports, and press materials.

2.12.5 Holders selected for examination shall be notified by a letter from the DOF's Audit Manager.

The following is an example of Notice of Examination letter issued by the State:

Dear [Holder Representative]:

Pursuant to §1171 of Title 12 of the Delaware Code, you are hereby notified that the State of Delaware intends to examine the books and records of [Company Name] and all of its Subsidiaries & Related Entities (hereinafter "[Company Name]"), to determine compliance with the Delaware Abandoned or Unclaimed Property Law, Title 12, Chapter 11, of the Delaware Code (the "Law"). The examination will relate to all property that may be subject to escheat pursuant to the Law. Abandoned or unclaimed property is reported to the State of Delaware pursuant to the Law, as well as the priority rules and other provisions set forth in the United States Supreme Court case Texas v. New Jersey, 379 U.S. 674 and 380 U.S.518 (1965) and reaffirmed by Delaware v. New York, 507 U.S.490 (1993).

The review will be conducted by Assigned Audit Firm ("AUDITOR NAME") on the behalf of the State of Delaware (the "State"). ("AUDITOR NAME") will contact you within the next three weeks to arrange a mutually agreed upon date to commence the examination. It is the State's expectation that an opening conference will be held within ninety days of this notice. In advance of the opening conference, ("AUDITOR NAME") will send you an initial document request seeking routine but necessary material which you are expected to produce at or before the opening conference. If [Company Name] desires ("AUDITOR NAME") to execute a confidentiality agreement, ("AUDITOR NAME") shall be promptly notified. The execution of a standard confidentiality agreement is permitted by Delaware regulations, but not required, and it shall not delay the opening conference. If [Company Name] believes that it cannot accommodate an opening conference within this timeframe, you should contact me immediately. The scope of the examination will be for the period of 10 years prior to when property is presumed abandoned under this chapter as of the date of this letter through the most recent reportable year due at the conclusion of the examination, or as otherwise agreed to by the State Escheator and the Holder. See 12 Del.C. §1172(h).

The State is hereby requesting that you issue a hold notice so that all records are retained, including, but not limited to, bank statements, bank reconciliations, outstanding check lists, detail general ledgers, aged accounts receivable reports, aged accounts payable reports, and if applicable, information surrounding gift card issuances and redemptions. The State requests that all records will be retained, notwithstanding any [Company Name] record retention policies to the contrary, until the examination is completed. See 12 Del.C. §1145. Your cooperation in making necessary records available for both past and present years for the purposes of determining [Company Name] compliance with the Law will facilitate the completion of the examination. In addition to specific document requests that will be forthcoming, please have available all of [Company Name] prior years' reports of unclaimed property and supporting documentation for all states, including Delaware. You will be advised throughout the course of the examination of what records will be required to complete the review.

If [Company Name] is presently working with or intends to retain a third-party consultant to assist [Company Name] in the conduct of this examination, please provide me with the name and contact information of the third-party consultant. As expressly stated in the Delaware regulations, the retention of a third party is no basis to delay the examination or the production of records.

In closing, you are specifically requested to have the appropriate individual in your organization contact ("AUDITOR NAME contact") of ("AUDITOR NAME") at (xxx) xxx-xxxx within three weeks of receipt of this notice in order to facilitate the exchange of prefatory information and to discuss scheduling of an opening conference.

If you have any questions about this notice, you may contact me at (302) 577-8776. Please be assured that, although ("AUDITOR NAME") is performing the examination as the State's agent, I am the final arbiter of any disputes that may arise during the course of the examination. I look forward to resolving this examination in an expeditious and cooperative manner.

Sincerely yours,

Audit Manager

2.13 Third-Party Advocates

2.13.1 Holders may retain third party advocates (the "Advocate") to assist them in the examination process. The retention of an Advocate is no basis to delay the commencement of the State's examination and the State will not delay the examination so that the Advocate may conduct a review or its own audit of the Holder's books and records in advance of the State's examination. The State will cooperate with the Holder and its Advocate and keep both of them apprised of records requests, interviews and the progress of the audit in general. All records will be requested directly from the Holder.

2.13.2 The State's examination shall not be limited to a review of work papers, compilations or record summaries prepared by the Holder or the Advocate, but shall include access to the Holder's original books and records deemed by the State to be necessary to ascertain the Holder's compliance with the Abandoned or Unclaimed Property Law. The State or the designated Auditor shall provide all requests and communications directly to the Holder and, if requested by the Holder, shall also direct copies to the Advocate.

2.13.3 The State and its Auditors shall keep Holder representatives directly informed of the progress of the examination. It is the responsibility of the Holder to make available to the State and its Auditors the employees most likely to have first-hand knowledge of the Holder's day-to-day operations. This minimizes the potential for delays caused by miscommunications, ensures the Holder understands its obligations, and aids in furthering future compliance.

2.13.4 The State shall conduct periodic reviews of the Auditors' conduct, processes, and procedures to ensure that the Auditors are complying with security protocols, record retention and destruction requirements, and all applicable statutes and regulations.

2.14 Confidentiality and Non-Disclosure Agreement ("NDA")

2.14.1 Holders have the opportunity to enter into a NDA with the assigned Auditor and may, but need not, use an NDA in a form approved by the State. If the Holder elects not to use an NDA approved by the State, and the Holder and Auditor cannot reach an agreement on the terms within sixty (60) days of the date of the Notice of Examination letter, the parties shall rely on the confidentiality provisions of 12 Del.C. §1189.

2.14.2 The State and its agents are prohibited from disclosing the amount of abandoned or unclaimed property that has been reported to and received by the State by any Holder and disclosing the terms of or supporting documentation related to any abandoned or unclaimed property annual filing, abandoned or unclaimed property VDA, or settlement agreement resulting from the reporting of any abandoned or unclaimed property.

2.14.3 The following is an example of a Non-Disclosure Agreement approved by the DOF (section 7 may be tailored to reflect the Auditor's specific security protocols):

CONFIDENTIALITY & NONDISCLOSURE AGREEMENT

This Confidentiality & Nondisclosure Agreement (the "Agreement") is made and entered this ___ day of _____________, 20___ by and between ___(AUDITOR NAME), a _____(STATE OF INC AND CORP FORM) company, ("_____________") and ________________________, a ________________, and its subsidiaries and related entities (collectively, the "Holder") (at times "_____________" or the "Holder" may be referred to as a "Party" and collectively as the "Parties").

1. Introduction. [AUDITOR NAME] is a contract auditor that has been authorized to conduct an unclaimed property examination (the "Examination") of the Holder by the state(s) identified on Exhibit A (hereinafter a "Participating State" or collectively, the "Participating States," and shall, upon written consent of the Holder, include any additional state or jurisdiction that may, during the course of the Examination, authorize [AUDITOR NAME] to act as its agent and to perform an unclaimed property examination of the Holder) to determine the Holder's compliance with the Participating State(s)' unclaimed property laws, rules, and regulations. Upon receipt of any subsequent examination authorization letter, [AUDITOR NAME] shall obtain written consent from the Holder to add such state to the list of participating states attached hereto at Exhibit A.

2. Confidential Information, defined. During the course of the Examination, [AUDITOR NAME] may have access to, or receive, confidential and/or proprietary information concerning the Holder including, but not limited to, materials relating to the administration of the Holder's business, operations, unclaimed property procedures and practices; financial information and/or accounting records; information regarding the Holder's current and former shareholders, members or partners, principals, directors, officers, employees, retirees, beneficiaries, customers, consumers, vendors, contractors, agents and other such representatives; and/or any other materials or information disclosed by the Holder or its principals, partners, directors, officers, employees, agents, consultants, advisors, legal counsel, accountants, and other such representatives (collectively "Representatives") to [INSERT AUDITOR NAME] and its Representatives in connection with the Examination. The Parties agree that all such information, including any materials derived therefrom, whether disclosed orally or in written (including electronic) form or otherwise, shall be considered proprietary and confidential and shall hereinafter be referred to as "Confidential Information". Confidential Information shall also include any report filing, voluntary self-disclosure agreement, or settlement agreement resulting from the Holder's reporting of any unclaimed property as well as any settlement, payment(s), or other interim or final resolution of the Examination. Confidential Information shall not include information or materials that are: (i) in the public domain not as a result of the violation of the undertakings herein; (ii) available to [AUDITOR NAME] on a non-confidential basis prior to the Holder's disclosure of it to [AUDITOR NAME], or (iii) hereafter made available to [AUDITOR NAME] on a non-confidential basis from a source other than the Holder, provided that such source in so acting is not violating any duty or agreement of confidentiality.

3. Non-Disclosure. [AUDITOR NAME], in receiving Confidential Information from the Holder or its Representatives, shall not disclose Confidential Information to any third-party (other than to representatives of other participating states to the extent provided below. [AUDITOR NAME] shall preserve the confidentiality of such Confidential Information and shall:

a. restrict disclosure of such Confidential Information to [AUDITOR NAME]'s Representatives having a "need to know" in connection with the Examination, and where such Representative is a third-party agent or contractor of [AUDITOR NAME], ensure that said Representative is either: (a) a party to a non-disclosure agreement sufficient to protect the Holder's legal and equitable right in the Confidential Information; or (b) under a duty of confidentiality with respect to the Confidential Information as a result of a legally binding, regulatory, or statutory prohibition. [AUDITOR NAME] shall be responsible for any breach of this Agreement by its Representatives;

b. advise its Representatives of the obligations of confidentiality hereunder with respect to the Confidential Information and ensure that its Representatives comply therewith;

c. restrict disclosure of such Confidential Information to Representatives of a Participating State(s) having a "need to know" in connection with the Examination, and only disclose that portion of the Confidential Information relative to such Participating State;

d. use such Confidential Information solely for the purpose of conducting the Examination on behalf of the Participating States, and not otherwise to (a) solicit any state or jurisdiction not listed on Exhibit A to investigate, undertake, initiate or conduct any unclaimed property examination of the Holder or to take any adverse action involving the Holder including, without limitation, any legal, regulatory, administrative, investigatory or any other action that involves the Confidential Information; and (b) appropriate such Confidential Information for [AUDITOR NAME]'s or its Representatives' own use or the use of any other person or entity;

e. maintain the confidentiality of the Confidential Information using efforts no less than those efforts [AUDITOR NAME] uses to maintain the confidentiality of its own Confidential Information of a similar nature and/or those efforts required under applicable federal, state and/or local law;

f. provide Holder with information regarding [AUDITOR NAME] security measures upon the reasonable request of Holder, including data security protocols with respect to any electronic file transfer process used for the examination;

g. prevent any disclosure of Confidential Information by its Representatives not otherwise permitted under this Agreement; and

h. not disclose or transfer Confidential Information outside the United States.

4. Solicitation. [AUDITOR NAME] shall not inform other states or jurisdictions that Delaware has authorized an examination of the Holder to solicit such states or jurisdictions to investigate, undertake, initiate or conduct any unclaimed property examination of the Holder. This restriction shall not, however, be construed to prohibit the Auditor from disclosing Delaware's involvement in the Examination to another Participating State once that state has issued a formal notice of examination to the Holder.

5. Records Retention. [AUDITOR NAME] shall retain the audit work papers (which may include the Confidential Information) in a secure environment for no longer than the period of time specified under the laws, rules or regulations of the Participating State(s) or [AUDITOR NAME]'s contract with the Participating State(s), whichever is longer, at which time the records (inclusive of any Confidential Information) shall be destroyed; and [AUDITOR NAME] shall certify in writing as to such destruction to the Holder using the following contact information:

Contact Name: ____________________________

Title: ____________________________

Company: ____________________________

Street Address: ____________________________

City, State, Zip ____________________________

Telephone Number: ____________________________

Email Address: ____________________________

6. Compelled Disclosure. If [AUDITOR NAME] shall be under a legal obligation, including but not limited to a subpoena or request by a court or any government entity or required in response to any applicable "freedom of information" request to disclose any Confidential Information to a third party, [AUDITOR NAME] shall give the Holder prompt notice thereof so that the Holder may timely object to the disclosure of such Confidential Information, seek a protective order, or waive [AUDITOR NAME]'s duty of non-disclosure. [AUDITOR NAME] shall reasonably cooperate with the Holder to the extent that it seeks a protective order or to otherwise object to the requested disclosure of the Confidential Information. Furthermore to the extent that the Holder seeks a protective order or objects to the requested disclosure and [AUDITOR NAME] is subsequently required to disclose by court order or governmental mandate any Confidential Information, or in the event Holder fails to act within a reasonable time period after receipt of [AUDITOR NAME]'s notice and/or affirmatively waives [AUDITOR NAME]'s duty of non-disclosure, and [AUDITOR NAME] is legally required to disclose any Confidential Information pursuant to this Section 6, [AUDITOR NAME] shall do so without liability under this Agreement.

7. Compliance With Applicable Laws. [AUDITOR NAME] represents and warrants that it has technical and organizational measures in place that (i) comply with all Applicable Laws; and (ii) meet or exceed the ISO/IECC 27002 information security controls standard to ensure the security and confidentiality of the Confidential Information in order to prevent, among other things: (a) accidental, unauthorized or unlawful destruction, alteration, modification or loss of the Confidential Information; and (b) accidental, unauthorized or unlawful disclosure or access to the Confidential Information. [AUDITOR NAME] warrants and represents that it shall maintain its security measures in accordance with: (i) the Applicable Laws; and (ii) the standards expressly represented in the INFORMATION SYSTEMS CERTIFICATION which is attached hereto and incorporated herein by reference at Exhibit B. For purposes of this Agreement, the term "Applicable Laws" shall mean all applicable state and federal laws, rules, and regulations governing the protection of Confidential Information (inclusive of Personally Identifiable Information) including, without limitation, 12 Del. Code Ann. §1189 and Del. Code Ann. tit. 6 §§ 12B-101 et. seq., as such laws, rules and regulations may be amended from time to time. In the event [AUDITOR NAME] is required to notify the Holder under any Applicable Law concerning any unauthorized access to, destruction, modification, disclosure or use of any Information (hereinafter a "Security Incident"), [AUDITOR NAME] shall: (a) provide such written notice promptly and without undue delay in accordance with the applicable legal authority; (b) take all remedial action required under Applicable Law to investigate and remediate any loss of the Information; (c) reasonably cooperate with Holder in promptly responding to all third party inquiries (if any) regarding the Security Incident; and (d) refrain from issuing any press release, providing any breach notification to individuals, or making any other public announcement concerning the Security Incident without the prior written approval of Holder (which approval shall not be unreasonably withheld, conditioned or delayed); provided, however, no written approval from Holder shall be necessary where [AUDITOR NAME] is required to act at the direction of law enforcement and/or other governmental personnel and such written approval is unreasonable under the circumstances and/or would result in [AUDITOR NAME]'s non-compliance with the directive.

8. Remedies. [AUDITOR NAME] hereby agrees that it shall promptly, and without undue delay notify Holder in writing of any unauthorized use or disclosure of the Confidential Information and reasonably cooperate with Holder to mitigate the effect of such unauthorized use or disclosure. [AUDITOR NAME] acknowledges that Holder would suffer irreparable harm if its Confidential Information were disclosed or used in violation of this Agreement, and that monetary damages would be an insufficient remedy for such unauthorized disclosure or use by [AUDITOR NAME] or its representatives. Accordingly, in addition to whatever right the Holder may have to obtain an award of damages or other relief upon [AUDITOR NAME]'s breach of this Agreement, the Holder may obtain an injunction or other equitable relief to protect its Confidential Information disclosed or used in violation of this Agreement.

9. Application of Agreement. This Agreement shall apply solely to the Examination and shall not be construed to permit the disclosure of any Confidential Information to any other state or jurisdiction not listed on Exhibit A on the date hereof, absent the express written consent of the Holder. This Agreement may not be canceled or modified, nor any of its provisions be waived, except in writing signed by the Parties hereto or, in the case of a waiver, on behalf of the Party making the waiver. This Agreement constitutes the entire agreement and understanding of the Parties hereto and supersedes any and all prior agreements and understandings relating to the subject matter hereof. If it is found in a final judgment by a court of competent jurisdiction that any term or provision hereof is invalid or unenforceable: (i) the remaining terms and provisions hereof shall be unimpaired and shall remain in full force and effect; (ii) the invalid or unenforceable provision or term shall be stricken from this Agreement and the validity, binding effect and enforceability of the remaining provisions of this Agreement shall not be affected or impaired in any manner.

IN WITNESS WHEREOF, the Parties have caused this Confidentiality & Non-Disclosure Agreement to be executed and delivered the day and year first above written.

[HOLDER NAME] [AUDITOR NAME]

its subsidiaries and related entities

2.15 Opening Conference

2.15.1 Once an examination is assigned, an opening conference shall be scheduled with the Auditor and representatives of the Holder. Prior to the opening conference, the Auditor shall provide the Holder a list of documents which the Holder must produce in advance of or at the opening conference. These documents may include but are not limited to the following: tax returns (including consolidated and affiliation schedules), organization charts, charts of accounts, trial balances, unclaimed property filing history (all states if the Holder is incorporated or formed in the State of Delaware), prior completed and accepted voluntary disclosure agreements (VDAs) and examinations, and policies and procedures related to record retention, accounting, unclaimed property, or any other practices the State deems relevant to the examination. During the opening conference, by way of example and not limitation, the Auditor shall

2.15.1.1 Advise the Holder of the reporting requirements of the Delaware Abandoned or Unclaimed Property Law;

2.15.1.2 Provide an overview of the examination process to include State approved methodologies, record availability, sampling and the potential for projection and estimation (if applicable);

2.15.1.3 Provide to the Holder an examination work plan;

2.15.1.4 Identify the maximum time-period to be covered by the examination, and discuss potential scoping issues;

2.15.1.5 Request additional records and materials necessary to proceed with the next steps of the examination, which may include, without limitation, the following: tax returns, unclaimed filing history for all states, bank statements, bank reconciliations, outstanding check lists, detail general ledgers, aged accounts receivable reports, aged accounts payable reports, and if applicable, information surrounding gift card issuances and redemptions.

2.15.2 Upon request by the Holder, the State shall provide to the Holder all records of prior unclaimed property reports filed previously in the State.

2.15.3 The State shall have access to the Holder's original books and records, or copies thereof, and will not limit its examination to a review of work papers, compilations or record summaries created by the Holder. The State expects the Holder's full cooperation and anticipates that, with the Holder's cooperation, the time to complete a typical examination shall not exceed twenty four (24) months.

2.15.4 If an examination lasts longer than 24 months, the Abandoned Property Audit Manager shall meet with the Holder to facilitate completion of the examination. Interest and penalties may be assessed pursuant to §§1183 and 1184 of the Abandoned or Unclaimed Property Law on all abandoned property due for all reporting years under examination.

2.15.5 Pursuant to 12 Del.C. §1185, in certain circumstances, interest and penalties may be abated for good cause at the discretion of the State Escheator. In determining good cause in this context, the State Escheator may consider, if applicable and without limitation, the following factors: whether the Holder has a significant history of filing unclaimed property reports; the responsiveness of a Holder during the examination; and whether the Holder used ordinary business care in its compliance efforts.

2.16 Scope of Examination

2.16.1 The scope of the examination may be dependent upon many factors, including but not limited to the following:

2.16.1.1 When an entity was incorporated, formed, or created;

2.16.1.2 When an entity began to engage in a particular line of business that may result in potential unclaimed property;

2.16.1.3 Activity/materiality;

2.16.1.4 Whether an entity was subject to a prior examination; and

2.16.1.5 Whether an entity completed, and the State accepted, a VDA.

2.16.2 Examinations may include all subsidiaries and related entities of the Holder under examination,

2.16.3 Once entity scoping has been determined by the State, no additional entities may be scoped into the examination without the Holder's consent.

2.16.4 At the Holder's election and with the consent of the State, legal entities acquired after the conclusion of entity scoping have the option of being added to the existing examination.

2.17 Examination

2.17.1 Depending on the facts and circumstances of the examination and in cooperation with the Holder, the Auditor may conduct the examination on-site and/or remotely if records are available electronically or can be shipped. When available in electronic format, records shall be produced electronically to maintain efficiency, absent exceptional circumstances to be determined by the State Escheator. On-site work may last a few days to several weeks depending on the size and complexity of the Holder, the availability of records, and the availability of Holder personnel necessary to explain and discuss the records. During the examination, the Auditor shall review all necessary books and records, interview key personnel and review relevant policies and procedures related to abandoned property.

2.17.2 During the examination, the Auditor may make subsequent requests to the Holder for additional books and records as required to complete the examination.

2.17.3 The State and/or its Auditors, shall retain copies of all examination source documents, work papers, and reports to create a suitable record for the judicial review procedure described in 12 Del.C. §1179, subject to the terms of any Non-Disclosure Agreement between the Holder and the Auditor.

2.17.4 Record requests shall have reasonable deadlines in order to move the examination forward and avoid unnecessary delays.

2.17.5 The Auditor shall submit record requests to the Holder in writing, or if the request is made verbally, shall follow up with written documentation of the request. The Auditor shall provide a reasonable timeframe for the Holder to respond to the request based on the type and extent of the information requested and other relevant facts and circumstances. The Auditors shall provide confirmation of receipt with projected response times to submissions received from the Holder. In turn, the Auditor shall provide to the Holder a reasonable timeframe for responding and reviewing records produced by the Holder.

2.17.6 During the pendency of the examination, if applicable and practicable, the Auditor shall provide to the Holder in writing:

2.17.6.1 Explanation of the process used to determine that items are unclaimed property;

2.17.6.2 Explanation of why documentation provided by Holder is not sufficient to remediate an item;

2.17.6.3 Explanation and support for determining the proposed assessment, including electronic copy of assessment and supporting schedules;

2.17.6.4 Explanation of steps Holder can take to remediate the assessment; and

2.17.6.5 The remediation timeline.

2.17.7 Holders shall be given the opportunity to review, reconcile, remediate and, where applicable under Delaware law, perform due diligence on any items that have been identified as potential unclaimed property. The Auditor shall verify that the Holder has mailed outreach letters (due diligence, remediation) to the owner's last known address. The Auditor shall conduct meetings with the Holder in order to provide guidance regarding the due diligence process and to ensure the Holder is performing the outreach within the timelines established by the State. The form of the outreach letter must be approved by the State, and all outreach letters shall be submitted to the Auditor for review and approval prior to sending out. See subsection 2.22 for examples of outreach letters in a form approved by the State.

2.17.8 The State may, at the Holder's request or with the Holder's agreement, bifurcate or divide the examination by property type and year. Thus, portions of an examination may be concluded while other portions remain ongoing. The State, through the Auditor, shall keep the Holder informed of any potential for such division to expedite the examination.

2.17.9 The Holder shall be kept informed of the progress of the examination and may contact the State directly to address issues or concerns. The Holder has the right to contact the State directly to address issues arising from or related to the examination, including the right to report alleged misconduct, unethical behavior, or lack of professionalism on the part of the Auditor.

2.17.10 At the end of any defined portion of the examination, the Auditor shall present the preliminary findings to the Holder. These findings are not final. The preliminary findings, at that point, identify in detail the work performed, property types reviewed, the time period reviewed, any estimation techniques employed, and a calculation showing the potential amount of unclaimed property due and owing. The Auditor shall allow the Holder reasonable time to complete required research and gather more records to address matters raised in the preliminary findings.

2.18 Estimation

2.18.1 Overview. Section 1145 requires that a Holder, who is required to file a report, retain records for 10 years after the date the report is filed. The record retention requirement corresponds with Section 1172(h) authorizing the State Escheator to conduct an examination for a 10 year period of dormant property. Section 1176 authorizes the State Escheator to estimate the amount of property due using a reasonable method of estimation based on all information available to the State Escheator.

2.18.2 Base Periods: The "Base Period" is the period of time for which the Holder possesses complete and researchable records. Consistent with a majority of states, the State requires that a Holder retain records for a minimum of 10 years plus dormancy (15 years total for most property types). It is expected that the Holder shall possess several years of dormant records even if the Holder does not possess records for the entire 10 year period. The State may utilize any available dormant records to estimate an unclaimed property liability for the period of time for which the Holder does not possess complete and researchable records.

2.18.2.1 If the Holder fails to retain sufficient dormant years of records, the Audit Manager and Holder shall discuss which records are to be utilized for the Base Period. In the absence of agreement, the State Escheator shall possess the sole authority to make a reasonable determination for the Base Period in order to prepare an estimate.

2.18.2.2 The Base Periods shall consist of complete and researchable records. In order to draw a representative error rate, the Base Periods utilized shall consist of at least three (3) years from the universe of complete and researchable records. Depending on the unique facts and circumstances of each Holder, the State may consider including non-dormant periods in the Base Periods.

2.18.2.3 At the conclusion of the records production, the Chief Financial Officer or other officer of the Holder shall provide in a form amenable to the State Escheator, a representation of the Holder to the best of his or her knowledge, after reasonable inquiry and due diligence, regarding what records are available, for which property types and what years. The Holder is bound by this representation, absent good cause in the determination of the State Escheator. A determination by the State of a false statement will be considered willful misrepresentation where it is made with intent to mislead the State Escheator.

2.18.3 Items to be Excluded from Estimation Calculation

2.18.3.1 Items payable to an owner that is a United States federal department or agency shall be removed from the population subject to estimation prior to preparing the population to review.

2.18.3.2 Funds returned in the normal course of business shall not be included in the population of potential unclaimed items.

2.18.4 Sampling

2.18.4.1 When it is determined through a documented discussion between the Auditor and the Holder that transactions for a particular property type meeting the State's parameters for testing constitute too large of a population to be reasonably tested on an actual basis, a statistical sampling methodology shall be employed.

2.18.4.2 If a Holder would prefer to research the entire population of a given property type and can perform the research in a reasonable time, the Holder shall be permitted to perform research of the entire population.

2.18.4.3 Generally, the population shall be divided into strata ("stratified sampling") from which samples shall be drawn. For each strata, a sample size shall be determined using generally accepted statistical principles such that the sample mean shall be within 10% of the population mean for that strata at a 90% confidence interval. However, in the instance of a lower valued stratum where the results are generally immaterial to the overall liability, a relaxed confidence and precision level intervals may be considered for purposes of efficiency, if accuracy is not sacrificed on a material level.

2.18.4.4 In some circumstances where the Holder has not maintained records for the entire examination period, the State may elect to sample a number of entities of a Holder during an examination in lieu of testing all Delaware entities. The Auditors shall identify an appropriate sampling of entities based upon factors such as, but not limited to, the following: revenue, line of business, commercial activity, and property types being held. The results of the detailed testing of these entities shall be extrapolated, if applicable, to the other appropriate Delaware entities that have not been selected for detailed review to determine the liability due to the State. The Holder shall be given the option to use this sampling methodology or to test all entities that fall within the scope of the examination.

2.18.4.5 The State's approved sampling process for estimating a Holder's unclaimed property liability includes the following steps:

2.18.4.5.1 Define the population

2.18.4.5.2 Determine appropriate stratification (if necessary)

2.18.4.5.3 Calculate Sample size

2.18.4.5.4 Perform random computerized sample selection

2.18.4.5.5 Verified achieved precision goals

2.18.4.5.6 Evaluate results

2.18.5 Funds Returned

2.18.5.1 The State shall review the Holder's policies and procedures for treatment of day-to-day operations related to potential unclaimed property.

2.18.5.2 For purposes of representing periods where records do not exist, the State shall consider the following:

2.18.5.2.1 Funds returned in the normal course of business will not be included in the population of potential unclaimed items.

2.18.5.2.2 Funds returned outside of the normal course of business (i.e. change in process) will be included in the population of potential unclaimed items.

2.18.6 Aging Criteria for Outstanding and Voided Checks

Checks that remain outstanding less than 90 days after issuance shall be excluded from the population, unless the State, in the sole discretion of the State Escheator, determines that a redefined outstanding period is necessary. A check that is voided within 30 days of issuance shall be excluded from the population, unless the State, in the sole discretion of the State Escheator, determines that a redefined outstanding period is necessary.

2.19 Projection

2.19.1 If for certain periods the amount of reportable property cannot be ascertained from the books and records of the Holder, projection techniques may be used to determine the reportable amounts for such periods. Such determination shall be made by first examining records during periods in which records exist to establish a "Base Period" of data from which statistical inferences can be made for periods in which records are incomplete or do not exist. To the extent permitted by law, names and addresses identified in the Base Period shall not be used to determine which state has the priority claim to the abandoned property estimated to be due over periods where records of owners' addresses do not exist.

2.19.2 All sampling, projection and estimation techniques used by the Auditor to determine unclaimed property due to the State shall be in a method approved by the State prior to use. The Auditor may suggest or the State may request, guidance necessary for the State to make an informed decision as to which estimation technique would be most appropriate for the facts and circumstances at hand. It is the intent of the State that any estimation methodologies used shall result in a reasonable representation of the unclaimed property potentially due for the estimated periods. The State shall permit the Holder to comment on or suggest an alternative technique; however, the ultimate decision to employ a particular technique is at the sole discretion of the State. The Holder may challenge this decision at the close of the examination.

2.20 Complete and Researchable Records

2.20.1 The expectation is that a Holder, at a minimum, may have complete and researchable records for a period that would cover seven to eight (7-8) years from the date of the Examination Notice. If there are unique circumstances where a Holder does not have 7-8 years of researchable records, the State and the Holder may discuss the circumstances and use an alternative data set with fewer years.

2.20.2 Complete records shall reconcile to the general ledger with the understanding that immaterial differences may occur. Researchable records are records to which the Holder may research the resolution of an item. At a minimum, researchable records shall include those items that contain a last known address of the owners of property.

2.21 Reportable Property Types

Commonly reported types of Unclaimed Property along with the National Association of Unclaimed Property Administrators ("NAUPA") Property Type Codes with Applicable Dormancy Periods are as follows:

NAUPA Code

|

ACCOUNT BALANCES

|

Property Type

|

Dormancy Period

(Years)

|

|

AC01

|

Checking Accounts

|

5

|

|

AC02

|

Savings Accounts

|

5

|

|

AC03

|

Mature CD or Save Cert

|

5

|

|

AC04

|

Christmas Club

|

5

|

|

AC05

|

Money on deposit to secure fund

|

5

|

|

AC06

|

Security Deposit

|

5

|

|

AC07

|

Unidentified Deposit

|

5

|

|

AC08

|

Suspense Accounts

|

5

|

|

|

|

|

|

UNCASHED CHECKS

|

|

|

|

CK01

|

Cashier's Checks

|

5

|

|

CK02

|

Certified Checks

|

5

|

|

CK03

|

Registered Checks

|

5

|

|

CK04

|

Treasurer's Checks

|

5

|

|

CK05

|

Drafts

|

5

|

|

CK06

|

Warrants

|

5

|

|

CK07

|

Money Orders

|

5

|

|

CK08

|

Traveler's Checks

|

15

|

|

CK09

|

Foreign Exchange Checks

|

5

|

|

CK10

|

Expense Checks

|

5

|

|

CK11

|

Pension Checks

|

5

|

|

CK12

|

Credit Checks or Memos

|

5

|

|

CK13

|

Vender Checks

|

5

|

|

CK14

|

Checks Written Off To Income

|

5

|

|

CK15

|

Other Outstanding Official Checks

|

5

|

|

CK16

|

CD Interest Checks

|

5

|

|

|

|

|

|

EDUCATIONAL SAVINGS ACCOUNTS (ESEA)

|

|

|

|

CS01

|

ESA - Cash

|

5

|

|

CS02

|

ESA - Mutual Funds

|

5

|

|

CS03

|

ESA - Securities

|

5

|

|

|

|

|

|

COURT DEPOSITS

|

|

|

|

CT01

|

Escrow Funds

|

5

|

|

CT02

|

Condemnation Awards

|

5

|

|

CT03

|

Missing Heir's Funds

|

5

|

|

CT04

|

Suspense Accounts

|

5

|

|

|

|

|

|

HEALTH SAVINGS ACCOUNT (HSA)

|

|

|

|

HS01

|

Health Savings Account

|

5

|

|

HS02

|

Health Savings Account Investment

|

5

|

|

|

|

|

|

INSURANCE

|

|

|

|

IN01

|

Individual Policy Benefits or Claim Payments

|

5

|

|

IN02

|

Group Policy Benefits or Claim Payments

|

5

|

|

IN03

|

Proceeds Due Beneficiaries

|

5

|

|

IN04

|

Proceeds from Matured Policies, Endowments or Annuities

|

5

|

|

IN05

|

Premium Refunds

|

5

|

|

IN06

|

Unidentified Remittances

|

5

|

|

IN07

|

Other Amounts Due Under Policy Terms

|

5

|

|

IN08

|

Agent Credit Balances

|

5

|

|

|

|

|

|

MINERAL PROCEEDS

|

|

|

|

MI01

|

Net Revenue Interest

|

5

|

|

MI02

|

Royalties

|

5

|

|

MI03

|

Overriding Royalties

|

5

|

|

MI04

|

Production Payments

|

5

|

|

MI05

|

Working Interest

|

5

|

|

MI06

|

Bonuses

|

5

|

|

MI07

|

Delay Rentals

|

5

|

|

MI08

|

Shut-in Royalties

|

5

|

|

MI09

|

Minimum Royalties

|

5

|

|

|

|

|

|

MISCELLANEOUS INTANGIBLE PROPERTY

|

|

|

|

MS01

|

Wages, Payroll, Salary (payroll cards)

|

5

|

|

MS02

|

Commissions

|

5

|

|

MS03

|

Workers Compensation Benefits

|

5

|

|

MS04

|

Payments For Goods & Services

|

5

|

|

MS05

|

Customer Overpayments

|

5

|

|

MS06

|

Unidentified Remittances

|

5

|

|

MS07

|

Unrefunded Overcharges

|

5

|

|

MS08

|

Accounts Payable

|

5

|

|

MS09

|

Credit Balance - Accounts Receivable

|

5

|

|

MS10

|

Discounts Due

|

5

|

|

MS11

|

Refunds Due

|

5

|

|

MS12

|

Unredeemed Gift Certificates

|

5

|

|

MS13

|

Unclaimed Loan Collateral

|

5

|

|

MS14

|

Pension & Profit Sharing

|

5

|

|

MS15

|

Dissolution or Liquidation

|

5

|

|

MS16

|

Miscellaneous Outstanding Checks

|

5

|

|

MS17

|

Miscellaneous Intangible Property

|

5

|

|

MS18

|

Suspense Liabilities

|

5

|

|

|

|

|

|

SECURITIES

|

|

|

|

SC01

|

Dividends

|

3

|

|

SC02

|

Interest (Bond Coupons)

|

3

|

|

SC03

|

Principal Payments

|

3

|

|

SC04

|

Equity Payments

|

3

|

|

SC05

|

Profits

|

3

|

|

SC06

|

Funds Paid to Purchase Shares

|

3

|

|

SC07

|

Funds for Stocks & Bonds

|

3

|

|

SC08

|

Shares of Stock (Returned by Post Office)

|

3

|

|

SC09

|

Cash for Fraction Shares

|

3

|

|

SC10

|

Unexchanged Stock of Successor Corp

|

3

|

|

SC11

|

Other Certificates of Ownership

|

3

|

|

SC12

|

Underlying Shares or other Outstanding Certificates

|

3

|

|

SC13

|

Funds for Liquidation / Redemption of Unsurrendered Stock or Bonds

|

3

|

|

SC14

|

Debentures

|

3

|

|

SC15

|

U S Govt Securities

|

3

|

|

SC16

|

Mutual Fund Shares

|

3

|

|

SC17

|

Warrant (Rights)

|

3

|

|

SC18

|

Mature Bond Principal

|

3

|

|

SC19

|

Dividend Reinvestment Plans

|

3

|

|

SC20

|

Credit Balances

|

3

|

|

|

|

|

|

TANGIBLE PROPERTY

|

|

|

|

SD01

|

SD Box Contents

|

5

|

|

SD02

|

Other Safekeeping

|

5

|

|

SD03

|

Other Tangible Property

|

5

|

|

|

|

|

|

FIDUCIARIES

|

|

|

|

TR01

|

Paying Agent Account

|

3

|

|

TR02

|

Undelivered or Uncashed Dividends

|

3

|

|

TR03

|

Funds held in Fiduciary Capacity

|

3

|

|

TR04

|

Escrow Accounts

|

3

|

|

TR05

|

Trust Vouchers

|

3

|

|

IR01

|

Traditional IRA - Cash

|

3

|

|

IR02

|

Traditional IRA - Mutual Funds

|

3

|

|

IR03

|

Traditional IRA - Securities

|

3

|

|

IR05

|

Roth IRA - Cash

|

3

|

|

IR06

|

Roth IRA - Mutual Funds

|

3

|

|

IR07

|

Roth IRA - Securities

|

3

|

|

|

|

|

|

UTILITIES

|

|

|

|

UT01

|

Utility Deposits

|

5

|

|

UT02

|

Membership Fees

|

5

|

|

UT03

|

Refunds or Rebates

|

5

|

|

UT04

|

Capital Credit Distributions

|

5

|

2.22 Remediation

2.22.1 Holders shall be given the opportunity to review, reconcile, remediate and perform remediation outreach on any items that have been identified as potential unclaimed property. The form of the outreach letter must be approved by the State, and all letters shall be submitted to the Auditors for review and approval by the State prior to sending out. The Holder must provide confirmation of the date of the outreach mailing to the Auditor.

2.22.2 For Property subject to the custody of the State pursuant to the Abandoned or Unclaimed Property Law, the following is an example of an outreach "due diligence" letter approved by the Department of Finance:

<Holder Letterhead>

<Date>

<Owner Name/Address>

Dear <Owner>,

Notice: The State of Delaware requires us to notify you that your property will be transferred to the custody of the State Escheator if you do not contact us before <insert date 30days after the date of this notice.>

The State requires us to make a diligent attempt to <renew contact with><reissue the property to> the owner. If contact is not renewed we are required to transfer your property to the custody of the State of Delaware. The State may sell property that is not U.S. legal tender. If property is turned over to the State, you may file a claim with the State for the return of the property or the proceeds of the sale.

Property Specifics:

Type of Property: ____________________ Account/Check No.: _______________

Amount: ___________________________ Date of last Contact: _______________

Any Additional Information: ______________________________________________________

To <reestablish contact> <receive your property>, you may sign below and return this letter ini the enclosed envelope to later than <insert # of days> from the date of this letter. Once we have the signed letter we will <restore your account to and active status><or reissue the property>. If you have any updated address information, please provide it in the space below.

Signature: _____________________________________________________________________

Title: ___________________________________ Date: ____________________________

Address (if new): _______________________________________________________________

Social Security # (last four) or Federal Tax ID Number (if applicable): ______________________

If you require additional assistance, please call us at <insert telephone contact and/or email>.

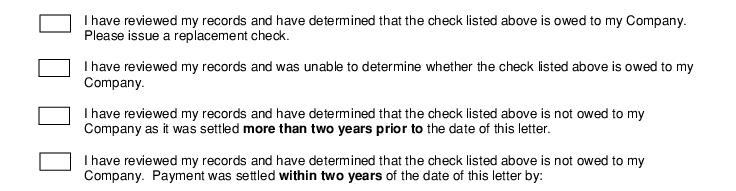

2.22.3 For Property utilized as part of the sampling or estimation process, the following is an example of an outreach "remediation" letter approved by the Department of Finance:

<Holder Letterhead>

<Date>

<Owner Name/Address>

Dear <Owner>,

Our records indicate that the check detailed below, issued to <Owner>, has not cleared the bank. In order for us to determine whether this obligation is still due and owing or whether the obligation may have been satisfied, we are requesting that you please review your records and respond back to us as to your findings. After reviewing your records, complete the form below and return it to us within 15 days. If your address has changed, please provide the new address as well as a telephone number.

If a response is not received, state unclaimed property laws may require us to remit the funds to the state of your last known address (i.e. the state listed on the address block of this letter). That state will hold the funds in perpetuity or until you claim the funds from the state.

Check Number Date Issued Invoice Invoice Date Amount

123456 04/04/2001 Inv 9999 03/15/2001 $250.00

Check the appropriate box below and return this confirmation to us:

receiving a subsequent payment on , or

through a settlement agreement on , or

through some other method on .

If other method, please explain and include all applicable dates:

Please sign here:

Print name and title here:

Business telephone number:

Address (if other than above):

Sincerely,

<Signature>

<Printed name of holder contact person> <Holder Phone Number>

<Holder Name>

<Holder Address>

2.23 Bankruptcy

If at any time before or during the course of an examination the Holder files for bankruptcy, the Holder shall give notice of the filing to the Auditor. The Auditor shall, within seven (7) calendar days of the Holder's notice or the discovery of the event, notify the State of the bankruptcy filing. If the State Escheator so elects, the Auditor shall assist the State Escheator to ensure that a proper proof of claim is filed timely in the bankruptcy action.

2.24 Statement of Findings and Request for Payment

2.24.1 If the Audit Manager determines at the conclusion of the examination that the Holder has not reported or has underreported the amount of unclaimed property due to the State, the State shall issue a statement of findings and request for payment to the Holder. This letter shall outline the findings of the examination and make a formal demand for the property under question. The Holder has ninety (90) days to directly remit to the State of Delaware any abandoned property identified during the examination as owed to the State of Delaware. The Holder's appeal rights to contest all or part of the findings as outlined in 12 Del.C. §1179 are triggered by the statement of findings and request for payment.

2.24.2 The State may, at the Holder's request and/or agreement, bifurcate or divide the examination by property type and year and issue a statement of findings and request for payment for a portion or portions of the examination while other portions of the examination remain ongoing. An examination is deemed to be complete for any category of property as of the date on which the Audit Manager mails the statement of findings and request for payment as described in 12 Del.C. §1179(a) for that category of property and time period. At the Holder's request, the State may provide a release and indemnification agreement for any categories of property where the examination is deemed to be complete pursuant to this Section.

2.25 Expedited Examinations

As provided in 12 Del.C. §1172(c), certain Holders may have the option of expediting the completion of a pending examination. The State shall publish a form "Intent to Expedite Completion of Examination" which shall outline the expectations of the Holder in that circumstance.